Mortgage Rate February 19, 2026

Hi friends, it’s Angela Simmons with Premier Homes by Angela — your trusted real estate and mortgage expert here in Georgia. 💕🏡

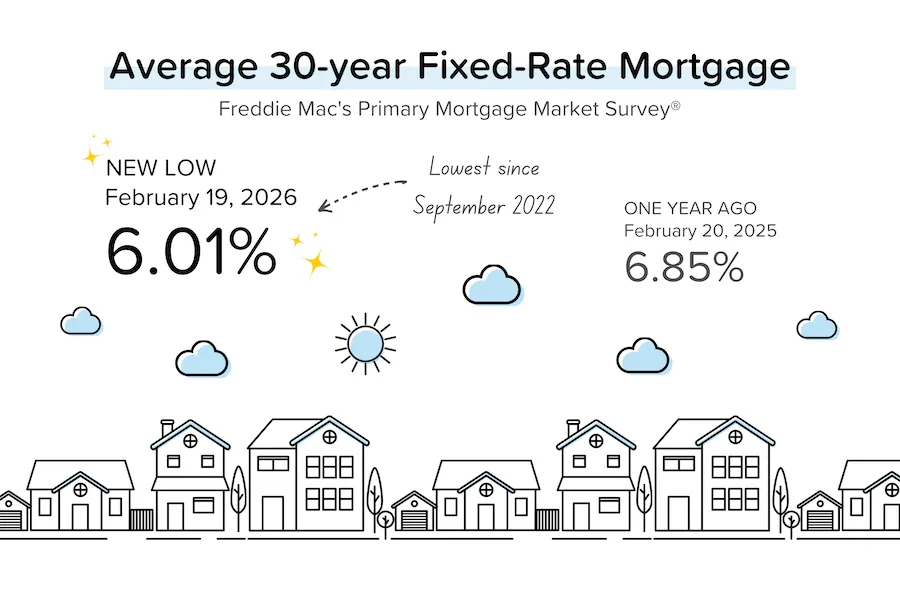

Mortgage Rates Drop to 6.01% — Lowest Since 2022

What It Means for Buyers and Sellers in Today’s Market

The housing market just received a notable shift.

After weeks of skepticism surrounding the recent “blowout” BLS jobs report, markets were surprised again — this time by a lower-than-expected CPI (inflation) reading. That softer inflation data revived conversations about potential Federal Reserve rate cuts in 2026.

And mortgage rates responded.

According toFreddie Mac’s Primary Mortgage Market Survey®, the average 30-year fixed mortgage rate fell to6.01%as of February 19, 2026 — the lowest level since September 2022.

For perspective, just one year ago, the average rate was6.85%.

That’s meaningful movement.

Rates Improved… But Sales Remain Soft

While borrowing costs have eased, buyer activity has not yet rebounded.

TheNational Association of Realtors® (NAR)reported that the Pending Home Sales Index for January 2026 declined 0.8% month-over-month to70.9— a new series low. This follows a sharp 7.4% decline in December 2025.

That may feel surprising considering mortgage rates are hovering near 6%.

NAR attributed part of the slowdown to severe winter weather impacting the Northeast and Southern regions. However, broader affordability concerns and consumer caution are still influencing buyer behavior.

What This Means for You

For Buyers:

Rates are at their lowest point in over three years.

Less competition may mean stronger negotiating power.

If rates decline further later this year, refinancing remains an option.

For Sellers:

Lower rates improve affordability and bring more buyers off the sidelines.

Inventory remains relatively tight in many markets.

Strategic pricing and strong marketing are critical in this cautious environment.

The Bigger Picture

The market is in transition.

Rates are improving. Inflation is cooling. The Fed may pivot.

Yet consumer confidence and affordability are still recalibrating.

This creates opportunity — but only for those who understand how to navigate it strategically.

If you’re considering buying, selling, or refinancing, this may be a window worth exploring.